FAQs on LTC Insurance and Your Taxes

By Mueller Financial Services, June 5, 2023

If you or a loved one needs long-term care (LTC) services, there are insurance products that can help cover the cost. As an additional incentive, qualified LTC policies deliver some tax advantages. For LTC policies, “qualified” means that a policy is offered by an insurance company licensed in your state and includes certain federal tax benefits. Here are some common questions about LTC insurance and its federal income tax effects.

How Does It Work?

Benefits paid under an LTC policy are often stated as daily maximums, typically ranging from $50 to $500. You choose the benefit level appropriate for your needs, and you’re reimbursed up to the amount chosen. An LTC policy with a monthly benefit reimburses you for a specified amount per month, regardless of how many days you receive care or the cost for those days.

You can buy an LTC policy with or without automatic annual inflation adjustments to your benefit maximums. Usually, the annual inflation adjustment rate is 3% to 5%, and that rate can be compounded annually or not. Not surprisingly, choosing a policy with an inflation adjustment feature adds to the cost.

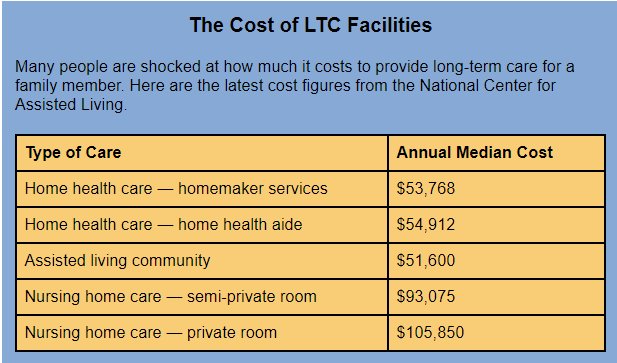

Lower benefits translate into lower premiums. But don’t get carried away with cost savings because long-term care can be expensive. (See “The Cost of LTC Facilities,” below.)

Benefit payments commence after the policy waiting period has been satisfied. A 90-day waiting period is typical. You may be able to choose benefit periods ranging from two years to lifetime coverage. Most policies have benefit periods of two, three or five years.

When Should I Sign Up for LTC Insurance?

When you sign up for LTC insurance, the hope is that you’ll pay fixed monthly premiums. The premiums are based on your age and health factors when you enroll. Enrolling at age 65 could cost quite a bit more than enrolling at age 55.

Your overall health must be reasonably good when you apply for coverage. Otherwise, you won’t be accepted regardless of your age. After you obtain coverage, it will remain in force — regardless of changes in health and advancing age — as long as you pay the premiums.

Important: While the LTC insurance company can’t raise your premiums due to changes in your age or health, it can raise premiums for broad classes of policyholders when a company’s financial results go south. For that reason, it’s important to check the overall reputation and premium-raising history of any insurance company you’re considering for LTC coverage.

Are LTC Insurance Benefits Tax-Free?

The general rule is that benefit payments received under a qualified LTC policy are federal-income-tax-free. Qualified policies must be guaranteed renewable, and they can’t have any cash value. Most LTC policies sold these days are qualified policies, but don’t sign up without first double checking.

Some qualified policies pay a designated daily benefit, regardless of actual costs. For 2023, benefits under such per-diem policies are automatically tax-free up to $420 per day. When benefit payments exceed the cap, they’re still tax-free if actual costs for qualified LTC services equal or exceed the payments.

For example, Betty’s LTC policy pays $500 per day regardless of actual expenses. If her actual expenses are $500 or more, she’ll have no taxable income from the payout. But if actual expenses are only $300 per day, she would have taxable income of $80 per day ($500 minus the $420 tax-free cap).

Important: Daily benefit payments are automatically tax-free if the insured person is terminally ill.

If you collect LTC insurance benefits during the year, the total amount will be reported to you on Form 1099-LTC, “Long-Term Care and Accelerated Death Benefits,” which you should receive early in the following year. The IRS will also receive a copy. Your tax advisor can help you calculate the taxable amount of your benefits, if any.

Can I Deduct LTC Insurance Premiums?

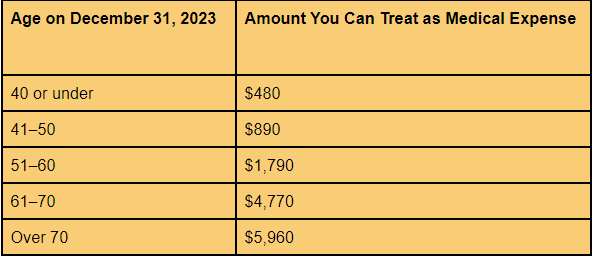

A qualified LTC policy is considered health insurance for federal income tax purposes. So, the premiums are treated as medical expenses for itemized medical expense deduction purposes. However, if your premiums exceed the annual age-based caps listed below, you can only count the capped amount as a medical expense.

Take your qualified LTC insurance premium amount (limited to the age-based cap if applicable) and combine that figure with your other medical expenses (health and dental insurance premiums, insurance co-payments, out-of-pocket prescription costs and all your other unreimbursed medical outlays). If the resulting total exceeds 7.5% of your adjusted gross income (AGI), you can write off the excess as an itemized medical expense deduction. This assumes that you have enough other types of deductions to itemize, rather than take the standard deduction.

AGI includes all taxable income items and is reduced by certain write-offs such as deductible IRA contributions and alimony payments required by a pre-2019 divorce agreement.

Don’t forget to count premiums paid for coverage on your spouse and any other dependent relative. For this purpose, a dependent relative is someone for whom you pay over half the cost of support during the year.

Important: If you’re self-employed, you can generally deduct premiums for qualified LTC insurance whether you itemize or not. However, the age-based deduction cap applies.

For More Information

As you get older, LTC insurance can provide much-needed peace of mind that you won’t become a financial burden on your family. LTC insurance premiums and benefits can also be eligible for favorable tax treatment. Contact us if you have additional questions about LTC insurance and its tax implications.

Copyright © 2023

long-term careRelated Insights

May 2, 2023

Podcast: 8 Questions to Consider Before Buying Life Insurance – A Needs Analysis

ShareMay 2, is Life Insurance Day, and marks the anniversary of the first day that life insurance became available in …

Read More navigate_next

March 21, 2023

Looking Into Long-Term Care Facilities

ShareThe need for long-term care assistance continues to grow. Roughly 5.8 million people in the United States used paid long-term …

Read More navigate_next