Pullback Perspective: The Reasons Why Stocks Are Pulling Back

By Mueller Financial Services, August 21, 2023

Volatility has returned right on cue as U.S. equity markets continue to pull back from overbought levels. The recent jump in interest rates has proven to be too much too fast for stocks to absorb, especially for the heavyweight and longer-duration technology sector. Deteriorating economic conditions in China and weak seasonal trends have been additional factors behind the selling pressure. However, don’t panic, pullbacks are completely normal within a bull market. With volatility comes opportunity, and as valuations reset, overbought conditions recede, and support is found, we believe a buying opportunity back into this bull market will present itself over the coming months.

Why are stocks pulling back?

Stocks are struggling this month as gravity appears to be setting in. While overbought conditions into August are part of the story, the recent jump in interest rates has captured most of the blame for the selling pressure. Benchmark 10-year Treasury yields have surged nearly 50 basis points (bps) over the last month, proving to be too much too fast for equity markets to absorb. This observation has been further evidenced by the correlation between 10-year yields and the S&P 500 recently turning negative for the first time since March.

Why are rates moving higher? Supply in the Treasury market is ramping up as the U.S. deals with an unwieldy budget deficit. The surge in supply comes at a time when the Federal Reserve (Fed) is reducing its balance sheet by limiting its ownership of Treasuries. Furthermore, inflation pressures abroad have kept rate hikes on the table for other central banks, while the Bank of Japan recently introduced greater flexibility to its yield curve control program. Finally, resilient economic data in the U.S. has reduced market expectations for an imminent recession, repriced longer-term inflation expectations higher, and pushed out rate cut expectations into next year, ultimately giving the Fed some leeway to keep rates higher for longer.

Rising rates have an even greater impact on longer-duration equities, including the technology sector. This sector—roughly a 27% weighting within the S&P 500—heavily relies on borrowing and future cash flows. As interest rates rise, the cost of capital also increases along with the discount rate, which lowers the present value of future cash flows. The technology sector also came into August well-extended above its uptrend and at a historically high valuation, so investors should not be surprised it is giving up some of its sizable gains this year and leading losses this month.

Of course, overbought conditions and rising rates can’t take all of the blame for the recent pullback. China, the world’s second-largest economy, has been the proverbial elephant in the room as investors wait for any signs of reopening momentum. However, despite continued policy support, economic conditions in China continue to deteriorate and weigh on the outlook for global growth. Record losses and a developing debt crisis in Country Garden, China’s largest property developer, have exacerbated contagion risk concerns within their troubled property sector. Unfortunately, economic risk goes well beyond the real estate market. Recent delinquent missed trust payments have shed new light on issues within China’s shadow banking sector (non-bank lending). As a result, and along with a string of disappointing economic data, the Hang Seng Index recently entered bear market territory after falling over 20% from its January high.

Where do stocks go from here?

Now that we know the primary reasons for the recent selling pressure in stocks, where do they go from here? As shown in Figure 1, the S&P 500 has pulled back from overhead resistance near 4,600 and violated a shorter-term uptrend. Overbought conditions are beginning to dissipate after the index reached a historically high 13% premium to its 200-day moving average (dma). The next major area of support sets up near the 4,200 to 4,300 range. We suspect this could be a logical spot for a rebound given the confluence of support in this area, record-high cash sitting in money market assets, and the fact that many investors missed the first-half rally. We view the 200-dma as a worst-case scenario for a drawdown.

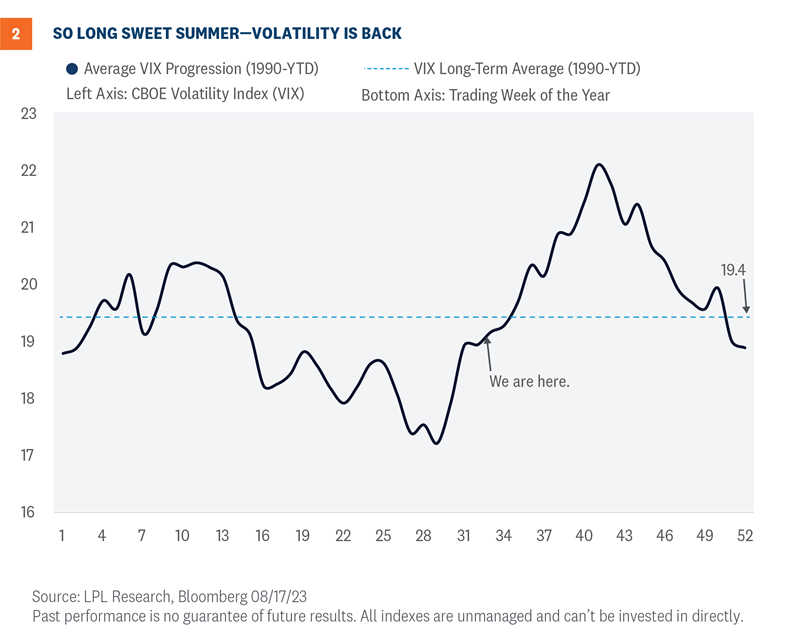

So long sweet summer

So long sweet summer as volatility is back in equity markets. After spending most of the year at well-below-average levels, the CBOE Volatility Index (VIX), or ‘fear-gauge’ as some prefer, appears to be mean reverting back toward its longer-term average. Although the VIX is trading higher, we have not seen the panic button pushed in the fear gauge, pointing to a relatively orderly pullback in the market thus far. And as shown in Figure 2, the uptick in volatility started right on queue as the VIX has historically bottomed in July before ramping up higher into the fall. This also coincides with weak seasonality trends for the S&P 500 during August and September.

Pullback scenarios

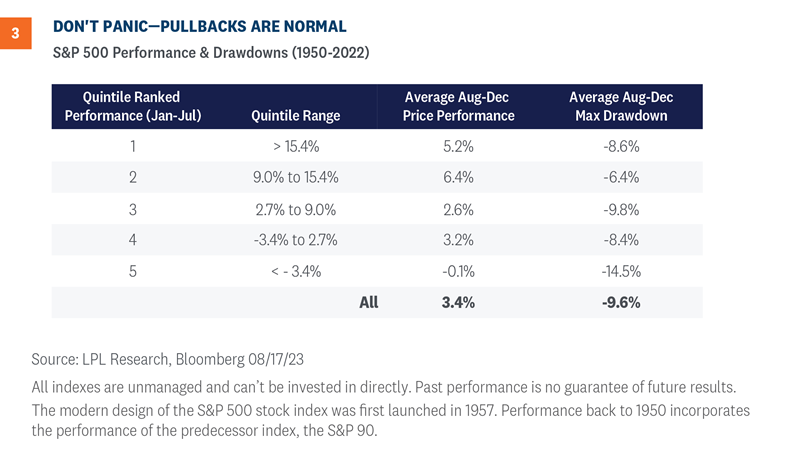

While overwhelming technical evidence supports the case for a sustainable longer-term bull market, expect some pullbacks along the way. The table below [Figure 3] compares intra-year price performance and maximum drawdowns for the S&P 500. At a high level, the table shows that even years with double-digit gains into August often experience sizable drawdowns over the remainder of the year.

To break down the data, we quintile ranked the performance of the S&P 500 from December 31 to July 31 for each year going back to 1950. We then analyzed the corresponding average returns and maximum drawdowns for the remainder of the year for each quintile group. With the S&P 500 up 19.5% as of July 31, this year falls into the top quintile. This group has gone on to post average August through December returns of 5.2% despite experiencing an average maximum drawdown of -8.6%.

Investment conclusion

Don’t panic, pullbacks are a normal occurrence within any bull market. We believe the depth of the drawdown will be limited to the 4,200 to 4,300 range on the S&P 500, with a worst-case scenario dip down to the rising 200-dma. Record-high money market assets, better-than-expected earnings, receding inflation, and a likely end to the Fed’s rate-hiking cycle should provide enough fundamental support for investors to buy the dip.

In terms of investment implications, we may see the 10-year Treasury yield above what we deem as fair value in the near term despite cooling inflation, before eventually settling back down in the mid-to-high threes if our forecast is right. A Fed pause is increasingly likely in September, which should help send rates down and prop up core bond returns.

LPL Research continues to like high quality fixed income despite upward pressure on rates recently. We think core bond sectors (U.S. Treasuries, agency mortgage-backed securities (MBS), and short-maturity investment grade corporates) are currently more attractive than plus sectors (high-yield bonds and non-U.S. sectors) with the exception of preferred securities, which look attractive after having sold off due to stresses in the banking system.

On the equity side, LPL Research believes stocks have moved a bit past what is justified by fundamentals in the short term and a 5-10% pullback is overdue.

Overall, LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) recommends a neutral tactical allocation to equities, with a modest overweight to fixed income funded from cash. Within equities, the STAAC recommends being neutral on style, favors developed international equities over emerging markets and large caps over small, and maintains the industrials sector as its top overall sector pick.

Adam Turnquist, CMT, Chief Technical Strategist

You may also be interested in:

- How This U.S. Debt Downgrade is Different from 2011 – August 14, 2023

- Key Earnings Season Takeaways –August 7, 2023

- A Cloudy Outlook Makes for Choppy Markets – July 31, 2023

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from Bloomberg.

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker -dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value |

RES-1606901-0723 | For Public Use | Tracking #1-05377714 (Exp. 08/24)

Related Insights

November 4, 2024

Election Stock Market Playbook

SharePrinter Friendly Version As Election Day approaches, we discuss potential stock market implications of various possible outcomes. But before we …

Read More navigate_next

October 28, 2024

What Scares Us About the Economy and Markets

SharePrinter Friendly Version Stocks have done so well this year that it’s fair to say market participants haven’t feared much. …

Read More navigate_next